Understanding the Financial Backbone of Most Businesses

Accrual Accounting is the standard method used by most profit-seeking enterprises to track income and expenses. It’s not just a technical term, it’s a powerful tool that helps businesses understand their true financial health by recognizing revenue when it’s earned and expenses when they’re incurred, not when cash changes hands.

How Does Accrual Accounting Work?

Imagine you run a business and you complete a project in September, but the client pays you in October. Under accrual accounting, you record the income in September, the moment you earned it. Not when the money hits your bank account. Similarly, if you receive a bill for services in September but pay it in October, the expense is recorded in September.

This method gives a more accurate picture of your business’s performance during any given period. It aligns revenue with the costs associated with earning that revenue, which is known as the matching principle.

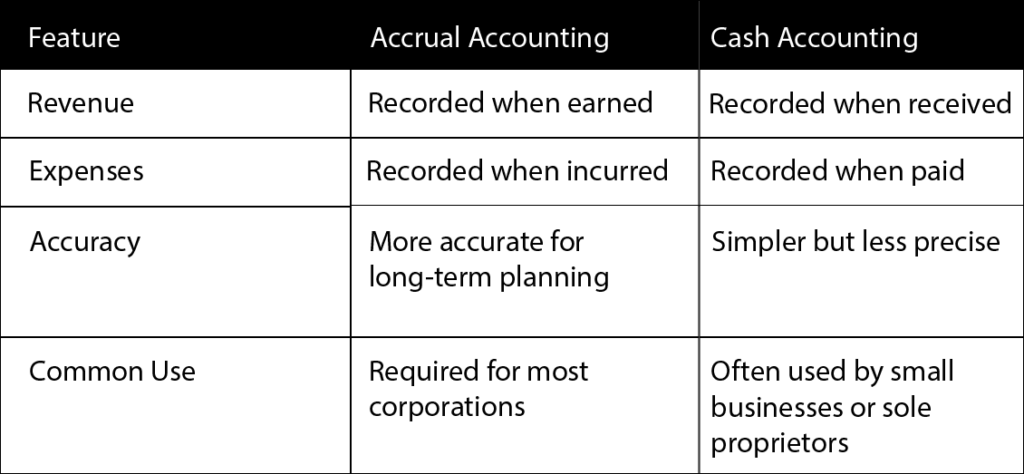

Accrual vs. Cash Accounting – What’s the Difference?

Cash accounting is straightforward. You only record transactions when money moves. It’s easier to manage but can give a misleading view of profitability, especially if you have unpaid invoices or upcoming bills.

Why Use Accrual Accounting?

Accrual accounting is especially useful when:

- You want to understand how profitable your business truly is.

- You have inventory, employees or complex transactions.

- You need financial statements that comply with Generally Accepted Accounting principles (GAAP), Accounting Standards for Private Enterprises (ASPE), International Financial Reporting Standards (IFRS).

- Your seeking investors or loans as they’ll want to see accrual-based financials.

It is not just compliance, it’s about clarity. Accrual accounting helps you make informed decisions, plan for growth, and avoid surprises.

When Should You Use Accrual Accounting?

If your business is growing, has multiple revenue streams, or you’re planning to scale, accrual accounting is likely the better choice. It’s also mandatory for incorporated businesses and those with revenues over a certain threshold in many jurisdictions.

If your business is growing, has multiple revenue streams, or you’re planning to scale, accrual accounting is likely the better choice. It’s also mandatory for incorporated businesses and those with revenues over a certain threshold in many jurisdictions.

How to Learn Accrual Accounting?

To begin learning accrual accounting, start by understanding the different types of accounts and how debits and credits affect them. These foundational concepts come together visually through T-Accounts and are easily remembered using the DEALER rule. Once you grasp these basics, you can begin applying them within the framework of the Generally Accepted Accounting Principles (GAAP). In Canada, these principles include ASPE (Accounting Standards for Private Enterprises) and IFRS (International Financial Reporting Standards). The choice between ASPE and IFRS depends on the type of business or organization and its specific financial reporting requirements. Future posts will explore each of these concepts in more detail.

{kind=link}